Open Enrollment has begun, so it’s time to choose your insurance policies to make sure you’re getting the best and most affordable coverage in the upcoming year. You have until December 15 to ensure your coverage for January 1.

How to Choose Insurance Coverage

If your job offers health insurance premiums, request the coverage information from human resources, or find them online. You need to compare premiums, copayments, deductibles, prescription costs, and out-of-pocket maximums in general and for various procedures. Some insurance providers require a specified percentage of procedures and visits. Others dictate that you pay a flat rate. Others still may have a combination of the two depending on the service given.

Family Plans

There are several types of plans offered by each insurance company. It may be common sense but, if you’re part of a family, only compare family plans. The individual coverage is usually the first type offered. Also, be sure to compare your coverage with your spouse’s employer-offered coverage. You will only need one family plan, and the benefits will vary by company.

If you’re expecting a child, planning to get married, or will have an elderly dependent, be sure to see if there are plans for multiple dependents. They will generally be more expensive but will cover your entire household.

PPO vs. HMO

Next, consider if you want to use a Preferred Provider Organization (PPO), Exclusive Provider Organization (EPO), or a Health Maintenance Organization (HMO). EPO and PPO plans are the same where there are facilities and healthcare providers included in your coverage network. However, and EPO may not cover your care outside of the network except in an emergency. With a PPO, you’re covered, but you may pay more out of pocket for the deductible or copayment. An HMO requires that all care goes through your primary care physician, including any referrals. The pricing structure is also different between the two types of coverage.

Location Changes

After you’ve figured how many people the plan covers, any preexisting conditions, then focus on any upcoming planned life events, such as moving to another state. Locations matter because your desired plan may not be available in every are. If you know you’re relocating, make sure your coverage will continue or find a plan that meets your requirements to switch to after your move.

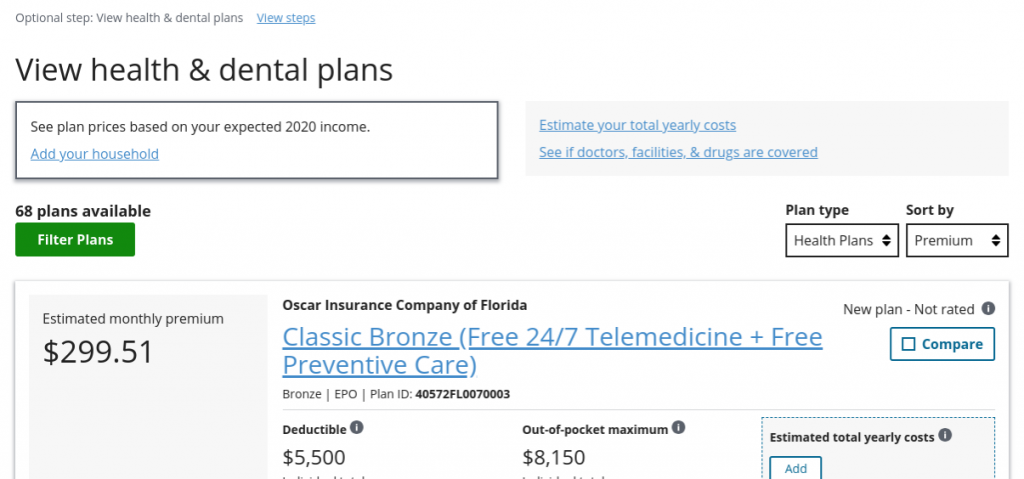

Choosing Insurance on Healthcare.gov

When you are using Healthcare.gov, the same practices apply. The website has a plan comparison chart you can use for review. Answer questions about your lifestyle and living situation and use filters to determine the best plan for you among the tiers and insurance companies provided. Or, you can skip the questions and preview all the coverage and prices for your zip code.

Health Savings Account

Some of the plans are eligible for a health savings account (HSA). You can save on taxes by using an HSA with Healthcare.gov or a health care flexible spending account (HCFSA) through an employer. The limits for the HCFSA have increased for 2020 by $50 to $2,750. The limits for the HSA has increased by $50 for individuals and $100 for families to $3,550 an $7,100, respectively. You can contribute pre-tax income up to the limit directly from your paycheck to reimburse you for healthcare costs, such as charges from a medical provider or prescriptions.

Read More